The Central Bank of Barbados will release its economic review for the first nine months of 2025 on Wednesday, October 29 at 11:00 a.m. The review will be live streamed on the bank’s Facebook and YouTube channels.

The blogmaster is of the view there is not enough relevant national discussions being had about the state of the economy. An activity that should be informed by our learned men and women on the Hill.

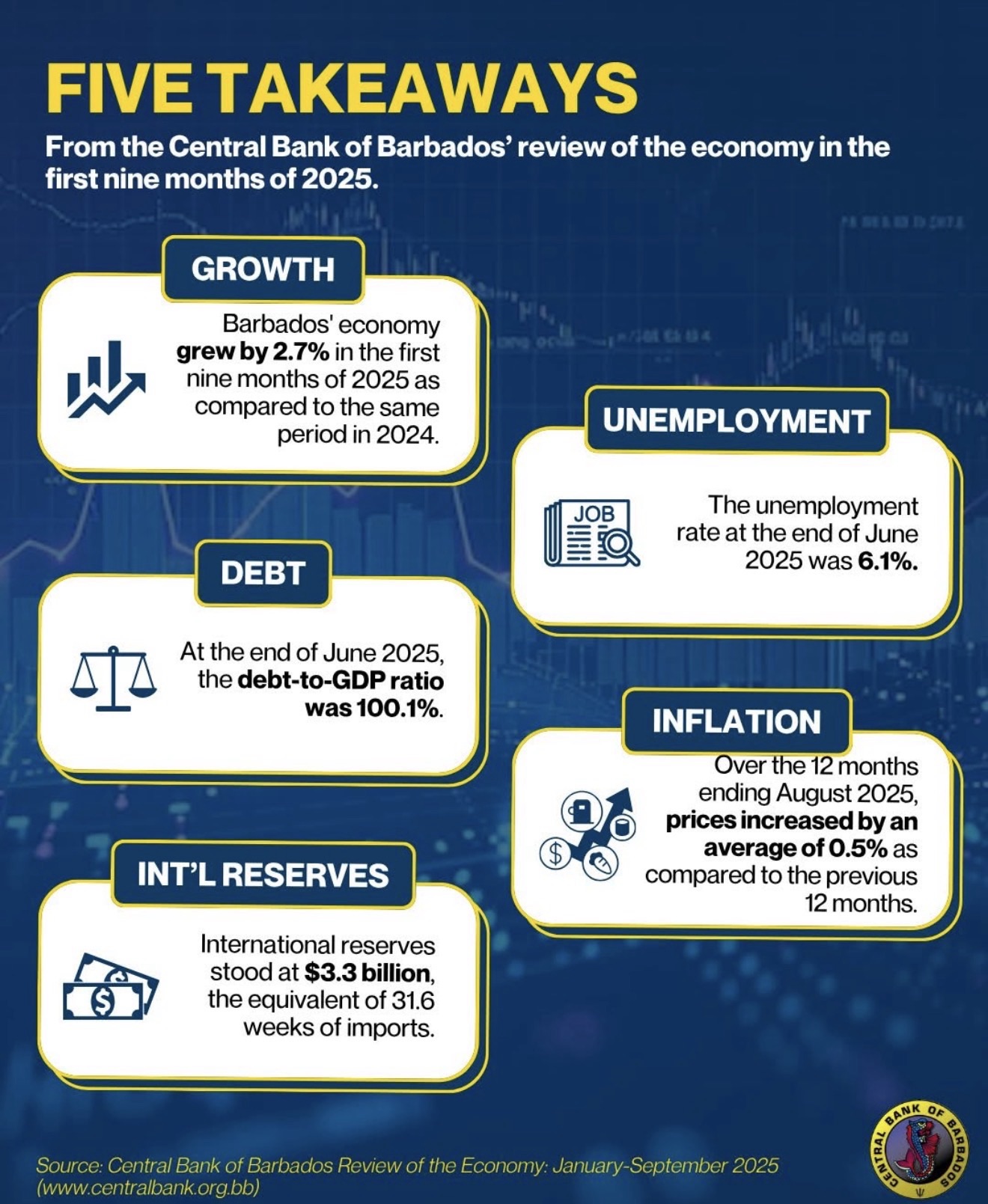

The debt to GDP graph for Barbados at first glance supports a boast by the Mottley led government. There is a steep descent from the high of 150% in 2017-2018 to a projected 102.8% by 2024-2025. However this visual masks structural fault lines in the economy we continue to ignore.

A reminder that the 2018 debt restructuring as a result of Barbados debt default is responsible for the significant decline in our debt to GDP. The domestic debt was reprofiled and bondholders took haircuts. The graph does not show the cost of the restructure WHITE OAK ADVISORY negotiated, however, there is no doubt investor confidence was negatively impacted in the domestic and international markets. The debt stock – as it is labeled by economists -was cosmetically altered, not reduced based on payback from earnings. The optics improved but the underlying liabilities have remained.

Our economic model is powered by the public sector, bloated and inefficient we know it to be. The government is the largest employer, the largest spender, and the slowest to implement projects. Productivity is stagnant, innovation is of little consequence. The private sector is largely parasitic, it feeds off government contracts and knockoffs from tourism.

The fickle tourism industry is our main engine of growth. It is one hurricane, one pandemic, one geopolitical flareup away from what Covid 19 showed us. Construction, the other ‘pillar’ is not sustainable. It is not export oriented, not foreign exchange earning. Also Barbados produces little the world wants, and imports almost everything. The foreign exchange reserves are therefore always under threat because of the fault lines in our economic model. We are therefore forced to borrow at usurius rates in the capital market because of our junk bond credit ratings.

Something we have mentioned in this space many times – Barbados operates a defined benefit scheme for public servants with payouts guaranteed regardless of economic conditions. The National Insurance Scheme (NISSS) is under pressure with pension obligations growing faster than revenue. These future liabilities are not adequately captured in the debt to GDP graph based on the blogmaster’s research.

The graph is simple to follow, although the debt to GDP trend line is heading in the right direction the fundamentals of the economy have not changed. The economy remains vulnerable, the debt remains high, and our economic model is not fit for purpose. This graph the blogmaster anticipates will continue to be used as a political tool to distract from the economic reality.

If we are to progress, our decision makers need to recalibrate our economic model. Are we to be satisfied with the placebo narrative and continue ignoring the disease our economic model endures? How long is too long if it hurts?

{kind=link}

The blogmaster invites you to join the discussion.