In recent weeks there has been noise in the traditional and social media space triggered by concerns coming out of the largest credit union in Barbados. It is no secret the blogmaster in the not too recent past registered concerns about how some matters were being managed at Barbados Public Workers Cooperative Credit Union (BPWCCUL) and subsidiaries, specifically CAPITA Financial.

It says a lot about the current state of member relations at BPWCCUL a few vocal members felt driven to share concerns in the public space. The blogmaster must admit a lot of the concerns are steeped in ignorance. Several of the few voicing concerns readily admitted to not having attended AGMs or having read relevant laws and rules governing how members should interact with the credit union it owns. For the purpose of this intervention the blogmaster will ignore those prominent persons from other credit unions seeking to ‘exploit’.

See Related Links:

- Concerned Barbados Public Workers Cooperative Credit Union Members Speaking Out

- Barbados Public Workers’ Co-Operative Credit Union Limited In Expansionist Mode

- Special Meeting Called By Concerned Group of Barbados Public Workers Cooperative Credit Union Ltd

- On The Ides Of March – BPWCCUL Has 14 Days To Respond!

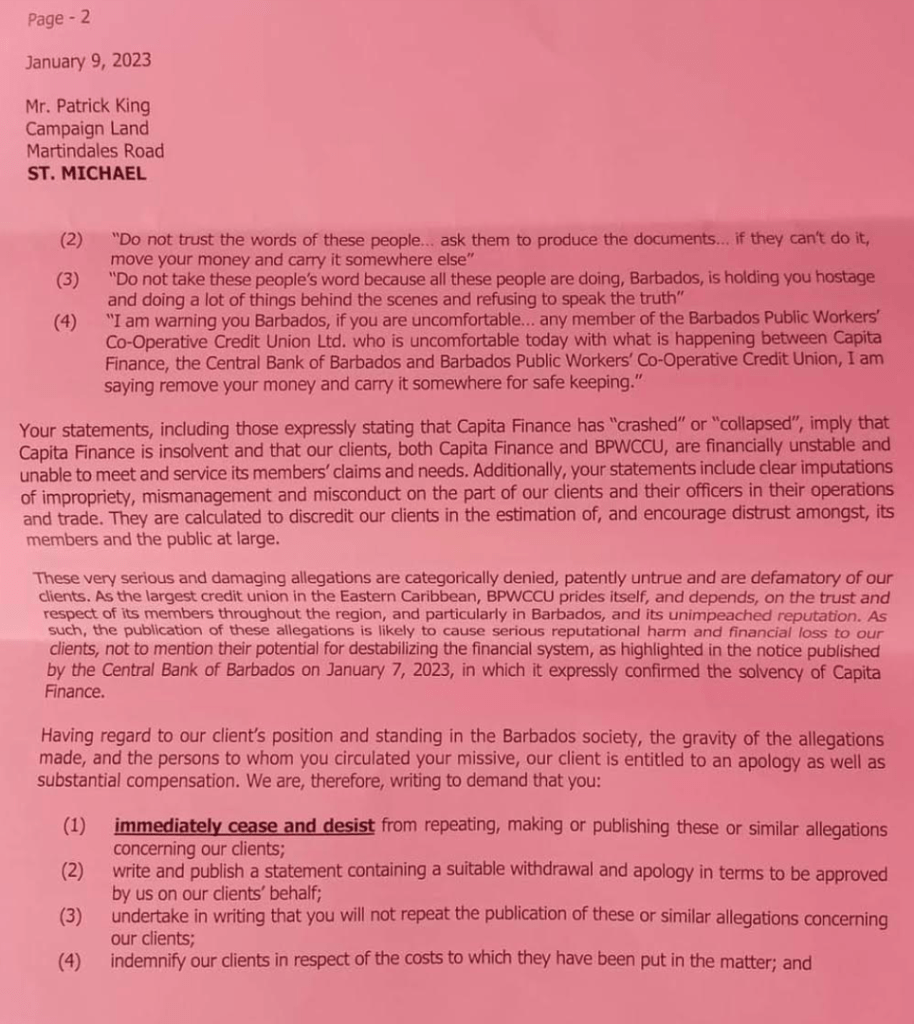

The BPWCCUL is not blameless to what is currently generating bad press and concerns from members. Having read BPWCCUL’s public statement on the matter and another by the Central Bank of Barbados, it is obvious the decision to refuse BPWCCUL’s subsidiary CAPITA an extension to filing 2022 financials and levying a fine of $18,000 could have been managed to achieve a better outcome. Was it reported the St. Lucia regulator approved an extension for the late submission of financials where CAPITA also operates?

The two local regulators in Barbados must be aware of a latent distrust by Barbadians of non bank financial institutions given the negative experience arising from Trade Confirmers, CLICO and a few others in recent decades. Why couldn’t the Central Bank of Barbados and Financial Services Commission approve the late submission conditional on providing an Action Plan to address issues that caused the problem by a specific date? As far as the blogmaster is aware this is the first time CAPITA missed the deadline for submission? Financial institutions are known to operate in a confidence sensitive environment and restoring confidence is not addressed by nicely worded public relations statements.

Not withstanding the above the blogmaster is concerned about the recycling of a few members from Board to Committees and Committees to Board who appear to control decision making at BPWCCUL and City of Bridgetown (COB). In fact it is a countrywide problem with members in ignorance ceding control of institutions AND country to a few who feed narrow interest.

To credit union members, you will get what you deserve if you ignore the opportunities provided in the governance process.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

The blogmaster invites you to join the discussion.