Submitted by Looking Glass

Economic theories of recession tend to focus on particular aspects of the problem and assume rationality. Financial history tells us that recessions are not new and will continue to occur. Like stock market crashes they all have to do with finance: the rise and fall in value of assets. The current global recession is not really a consequence of increasing interest rates and rising inflationary pressures but appears rooted in the real estate collapse and its interlinkages with the credit market.

Politicians propose and put in place policies to prevent recessions. But not infrequently such policies, though well intentioned, have had devastating consequences. Something is suspect about a solution which is always considered logically correct despite the problem.

The Wall Street crash of 1929-32 led the automobile industry to lay off ½ of its workforce. The unemployed gathered at the Ford plant to request unemployment relief. A scuffle occurred with security in which five were killed. This led to the building of homes in the eight mile district on one side of the “WALL.”

The US government as part of the New Deal Reform—Fannie Mae and later Freddie Mac in 1981— underwrote the mortgage market, and by reducing the monthly cost facilitated the explosion of home ownership. But the homes were not for everyone. To qualify for loans from the Federal Housing Authority developers built homes in Detroit on the white side of the WALL. Blacks were deemed to be predominately uncredit-worthy and denied property ownership. The few who could afford it had to pay higher interest rates and meet other requirements. Government policy, in this case credit, separated the city by colour/race, later the country by credit rating and the Prime and Subprime as we know it today

Blacks exclusion from home ownership led to the civil rights struggle and rioting in 1967 during which homes were damaged or destroyed and 43 killed. Later the government took over the properties being built on the wrong side, the black side of the Wall. Excused from credit worthiness blacks were offered incentives including more accessible loans. Mortgage lenders offered all kinds of deals to borrowers the vast majority of whom were renters and Subprime. After 1981 mortgages moved from a fixed 30 year term to low interest only rate payments and shorter duration.

Houses became commercial assets promoted by the real estate market as an investment. In the interim manufacture (value added) which had been in decline for at least the last 40 years was replaced by a largely unregulated finance industry which unlike manufacture created few jobs. The economy became guided not by the business cycle but by the consumer cycle.

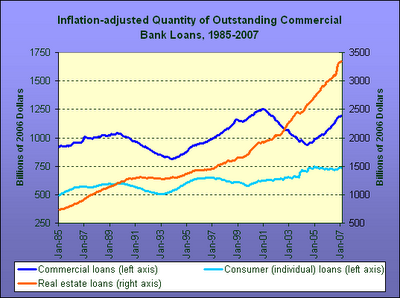

Liberal lending practices also gave birth to Securitization. Subprime lenders sold the loans to banks who split, bundled and repackaged them, had them rated AAA and sold them at home and abroad. Securitization and the credit market fed the global crisis. By 2003 the USA had accounted for 90% of worldwide securitization issuance.

Total volume of mortgage by government agencies grew from $370 bn in 1985 to $2.5 trillion in 2000 and was estimated to top $4 trillion in 2007 (Bad Money 115). People bit off more than they could chew, but the model worked well as long as people had jobs, interest rates remained low, property values continued to rise and the market self-corrected. But this was not the case. The percentage of household disposable income spent on debt service—credit card debt, car loans etc.—rose appreciably and weakened the masses. Home owners were indeed vulnerable to changing economic times, rising interest rates and other costs. But in case of default and foreclosure the lenders deficits were guaranteed even if the banks went bust.

The housing sector — mortgage finance but construction, furnishing, lumber and related industries — together represented ¼ of the GDP and unemployment. So the real estate slump was sure to foster significant dislocation. The Subprime market soured in 2007 sending shockwaves throughout the financial markets and worldwide. In 2008 Fanny Mae and Freddie Mac was nationalized to avoid collapse of the mortgage market. It cost the surviving institutions millions.

Government fiscal policy and liberal lending practices created the Prime, Subprime and securitization which fed the global crisis. Subprime loans led to default and foreclosure, the induced s credit crunch led to the stock market crush, and securitization fed the global crisis. But it is not over yet. Last year one in 45 households received a foreclosure filing. Today about one in five home owners with a mortgage owe more that their home is worth. And most banks have resumed their eviction process. The worst is yet to come.

The recession is a reminder that even if deviations are random markets do not self-correct or tend toward equilibrium

PS: Does the government really intend to support certain interests in the by-election as presently constituted? Fallacy in Shoddy Robes asked if they were things to hide or kept hidden. As you now very well know some Candles Under The Bed are no longer hidden. It is not too late to change ‘strategy.’ When it rains it pours. Stay tuned.

The blogmaster invites you to join the discussion.