The following blogs authored by a young Barbadian Economist Simon Naitram who is currently an assistant lecturer at the University of the West Indies while pursuing a PhD from the University of Glasgow (featured image: Simon Naitram)

- David, Barbados Underground

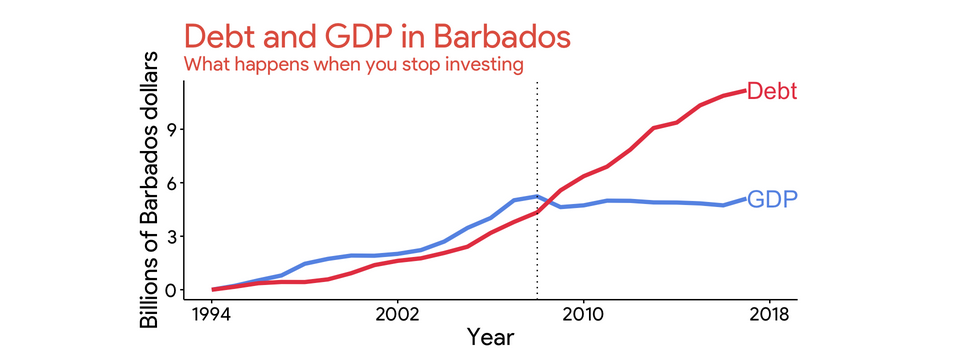

Life, debt, and now default. Barbados has reached the final stage of its illness. This isn’t our sob story. This is the tale of how we got here. This post isn’t a eulogy—it’s a lesson, a warning to our future selves.

The reason the government has defaulted on the country’s public debt is simple: the government just doesn’t have enough money to both keep paying back its loans and keep the country’s services running. The government chose to keep the country running.

How did the government reach this breaking point? Did the government simply borrow more than it could repay? The economics of government debt aren’t that simple. The government might have borrowed too much—it certainly made some bad financial decisions—but that’s not the real economic story.

The underlying economic mistake leading to default is that our government did not invest. It’s not that we spent too much money. Instead it’s that we spent our money on the wrong things. For a decade we did not invest in a brighter future. Nodebtw that we’ve reached that future, it’s a dark and miserable place.

A government’s debt is measured relative to how rich its people are. Bill Gates borrowing a million dollars isn’t the same as me borrowing a million dollars. The richer we the people are, the more money the government gets from taxing us. A 20% tax on $100 gives the government way more revenue than a 20% tax on $20.

Read full text – Life, Debt, and Default

Barbados’ giant economic hole is entirely of our own making. Our distress stems from one fatal flaw: we do not invest.

Let me make it plain. Investment in new businesses, new technologies, and new ideas is the only way to generate sustainable economic growth. Economic growth is not just an economist’s foolish cravings. Economic growth is the only path to prosperity. Investment is needed for economic growth, and without economic growth, we perish.

Why is it that we don’t invest? What can we do to fix this fatal flaw?

The first problem is that we save only 13.6% of our income. The rest of the world saves 23.1% of its income. Our savings are paltry in comparison to the investment hole we need to fill. We simply don’t put aside enough money for our businesses to invest.

And yet, commercial banks don’t want our cash. They offer us a ridiculous 0.05% interest rate on our savings. Why? In 1990, the banks lent 68% of our savings to businesses. Lending to businesses is risky, but it is productive investment that generates high returns and grows the economy. In 2018, the banks have lent only 28% of our savings to businesses! Banks have stopped channeling our funds into productive economic activity—which is in fact their one job.

Read full text – Failure to Invest

The blogmaster invites you to join the discussion.